New Mountain Finance Stock: Defensive BDC On Sale (NASDAQ:NMFC)

ipopba/iStock by using Getty Illustrations or photos

New Mountain Finance (NASDAQ:NMFC) is a company improvement enterprise with a increasing and very well-managed portfolio, floating publicity that signifies higher portfolio revenue as interest fees rise, and a minimal non-accrual level.

On top of that, the business enhancement enterprise addresses its dividend payments with net investment decision revenue, and the inventory now trades at a 13% discount to reserve benefit. The stock is interesting to dividend buyers seeking large recurring dividend money, although NMFC’s lower valuation relative to reserve worth leaves area for upside.

Purchasing A 10% Yield At A Discount

Less than the Investment decision Corporation Act of 1940, New Mountain Finance is labeled as a Small business Development Firm. The BDC is managed externally, which suggests it pays one more firm for administration companies. New Mountain Finance generally invests in middle-marketplace firms with EBITDA of $10 to $200 million.

The majority of New Mountain Finance’s investments are senior secured financial debt (1st and next lien) in industries with defensive features, which implies they have a higher probability of doing properly even in recessionary environments. New Mountain Finance’s main company is center market place credit card debt investments, but the business also invests in internet lease attributes and fairness.

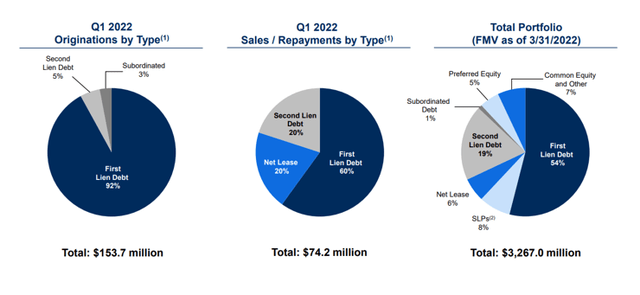

As of March 31, 2022, New Mountain Finance’s portfolio was composed of 54% 1st lien debt and 19% next lien financial debt, with the remainder distribute throughout subordinated debt, fairness, and internet lease investments. In the initial quarter, virtually all new mortgage originations (92%) were being very first lien personal debt.

The whole exposure of New Mountain Finance to secured to start with and 2nd lien personal debt was 73%. As of March 31, 2022, the company’s whole portfolio, together with all credit card debt and fairness investments, was $3.27 billion.

Portfolio Summary (New Mountain Finance Corp)

Curiosity Fee Publicity

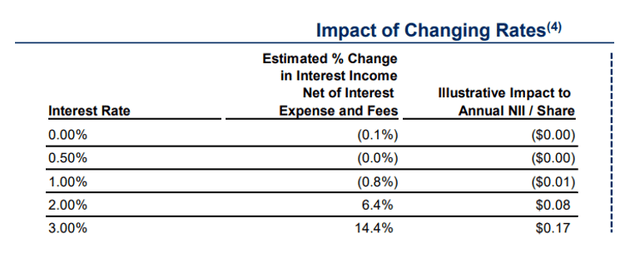

New Mountain Finance has taken treatment to make investments primarily in floating rate credit card debt, which guarantees the investment decision business a financial loan fee reset if the central lender raises desire fees. The central bank raised curiosity costs by 75 foundation points in June to overcome mounting inflation, which hit a 4-10 years high of 8.6% in May possibly. An boost in benchmark interest fees is expected to outcome in a important boost in internet interest profits for the BDC.

Effects Of Shifting Premiums (New Mountain Finance Corp)

Credit Performance

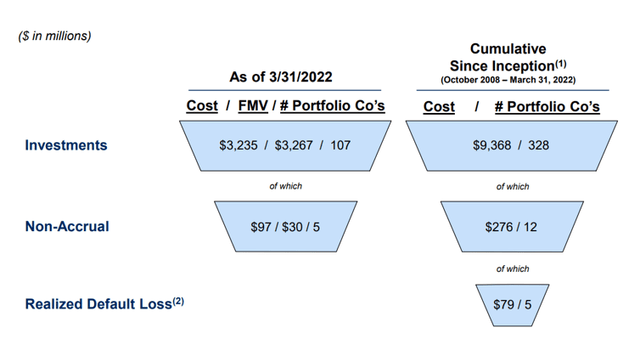

The credit score general performance of New Mountain Finance is excellent. As of March, 5 of 107 companies were being non-accrual, representing a $30 million fair value publicity. Considering that the BDC’s full portfolio was really worth $3.27 billion in March, the non-accrual ratio was .9%, and the enterprise has however to acknowledge a loss on those people investments.

Non-Accrual Ratio (New Mountain Finance Corp)

NII Addresses $.30 For each Share Quarterly Dividend Spend-Out

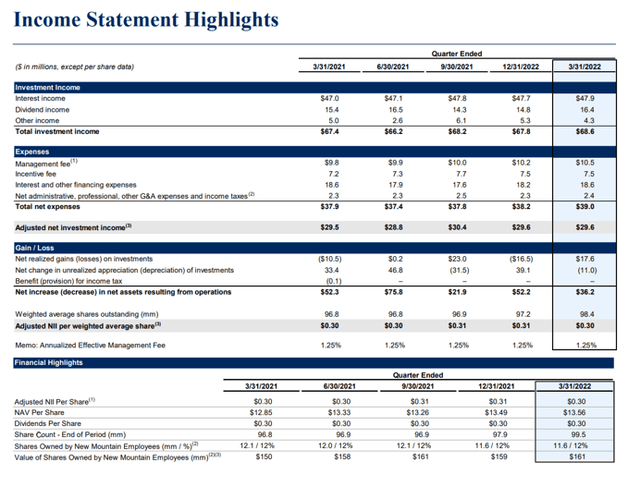

New Mountain Finance’s dividend of $.30 for every share is covered by adjusted web financial investment revenue. In the former calendar year, New Mountain Finance experienced a shell out-out ratio of 98.4%, indicating that it has continually included its dividend with the earnings created by its personal loan investments.

Even although New Mountain Finance now handles its dividend with NII, a deterioration in credit score high quality (loan losses) could lead to the BDC to below-receive its dividend at some stage in the future.

Revenue Assertion Highlights (New Mountain Finance Corp)

P/B-Numerous

On March 31, 2022, New Mountain Finance’s e-book worth was $13.56, whilst its inventory rate was $11.84. This indicates that New Mountain Finance’s expenditure portfolio can be obtained at a 13% price reduction to reserve value.

In the latest weeks, BDCs have begun to trade at bigger bargains to guide worth, owing to issues about rising desire costs and the probability of a economic downturn in the United States.

Why New Mountain Finance Could See A Lower Valuation

Credit history high quality and guide benefit trends in business enterprise improvement providers demonstrate investors whether or not they are working with a reliable or untrustworthy BDC. Firms that report lousy credit quality and reserve price losses are frequently forced to cut down their dividends. In a downturn, these BDCs need to be averted.

The credit rating high-quality of New Mountain Finance is strong, as measured by the stage of non-accruals in the portfolio. Credit rating high-quality deterioration and ebook price losses are chance aspects for New Mountain Finance.

My Conclusion

New Mountain Finance is a well-managed and cheap business progress corporation to devote in.

At the moment, the inventory rate is decrease than the NMFC’s book value, implying that the BDC can be purchased at a 13% price reduction to e book price.

In addition, New Mountain Finance’s overall credit rating quality seems to be favorable, and the company enhancement firm covers its dividend payments with web investment decision cash flow.