Here’s What to Expect Ahead of Analyst Day

Next Thursday (June 9), State-of-the-art Micro Units (AMD) will maintain its Analyst Day, the to start with these party because March 2020.

That could only be 2 a long time in the past, but a lot has adjusted in the interim the entire world is now on the other aspect of a global pandemic and confronted with a whole new set of worries with the prospect of a recession pretty true.

In the meantime, in spite of struggling like most other people in 2022’s unstable inventory marketplace, AMD has additional cemented its place as a correct chip big. As Deutsche Bank’s Ross Seymore puts it, “The power of AMD’s execution given that its March 2020 Analyst Working day are not able to be understated, as evidenced by the organization ultimately beating Street 2021 profits estimates by ~+60% and EPS estimates by +75%.”

The outsized gains are down to a combination of sector-large and enterprise-distinct “tailwinds.”

For the former, see the pandemic-pushed desire for Laptop/gaming and “strength” in Details Centre paying. For the latter, astute management has steered the organization superbly while AMD has also been speedy to pounce when largest competitor Intel has stumbled. It has due to the fact shut the hole concerning the two organizations substantially. The result is a market cap that has more than doubled since the previous Analyst Day.

So, what to seem forward to at the function? Seymore expects AMD will “rightfully exhibit ongoing self confidence in its long run expansion likely,” whilst there are now more “moving parts” to take into consideration. These include the addition of more recent “product offerings” (XLNX, Pensando) and an natural environment the place competitiveness has intensified beyond the rivalry with just Intel.

A comparatively thorough roadmap detailing the designs for different segments – Details Center, PCs, Gaming, and Embedded – must also be delivered, and just one which will tension the “differentiations” in comparison to the merchandise introduction ideas issued by Intel previously this year.

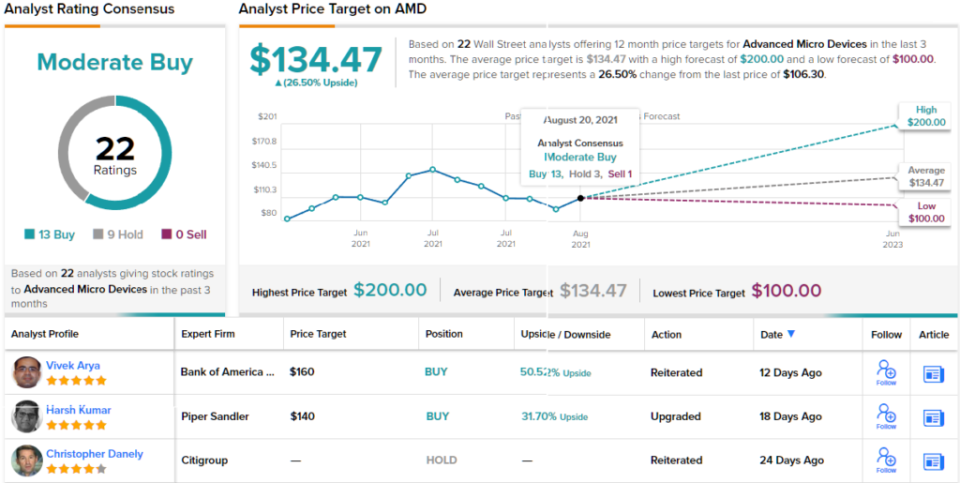

That explained, in spite of expecting “continued powerful profits growth and sound profitability improvement” more than the extensive expression, the developing competitiveness (Nvidia, Intel, ARM-dependent and so on), ongoing problem in achieving “incremental share gains,” and the in general “risk off” current market method pertaining to growth names, are why Seymore has a Keep (i.e. Neutral) score for the shares. (To look at Seymore’s keep track of record, click listed here)

Overall, 8 other analysts be a part of Seymore on the sidelines, but with an more 13 Purchases, the inventory promises a Average Get consensus rating. Heading by the $134.47 common goal, the shares are predicted to climb 26.5% better around the coming year. (See AMD stock forecast on TipRanks)

To discover very good ideas for shares buying and selling at eye-catching valuations, stop by TipRanks’ Finest Shares to Buy, a freshly introduced resource that unites all of TipRanks’ fairness insights.

Disclaimer: The thoughts expressed in this report are exclusively these of the showcased analyst. The written content is meant to be made use of for informational reasons only. It is incredibly critical to do your have investigation in advance of making any expense.